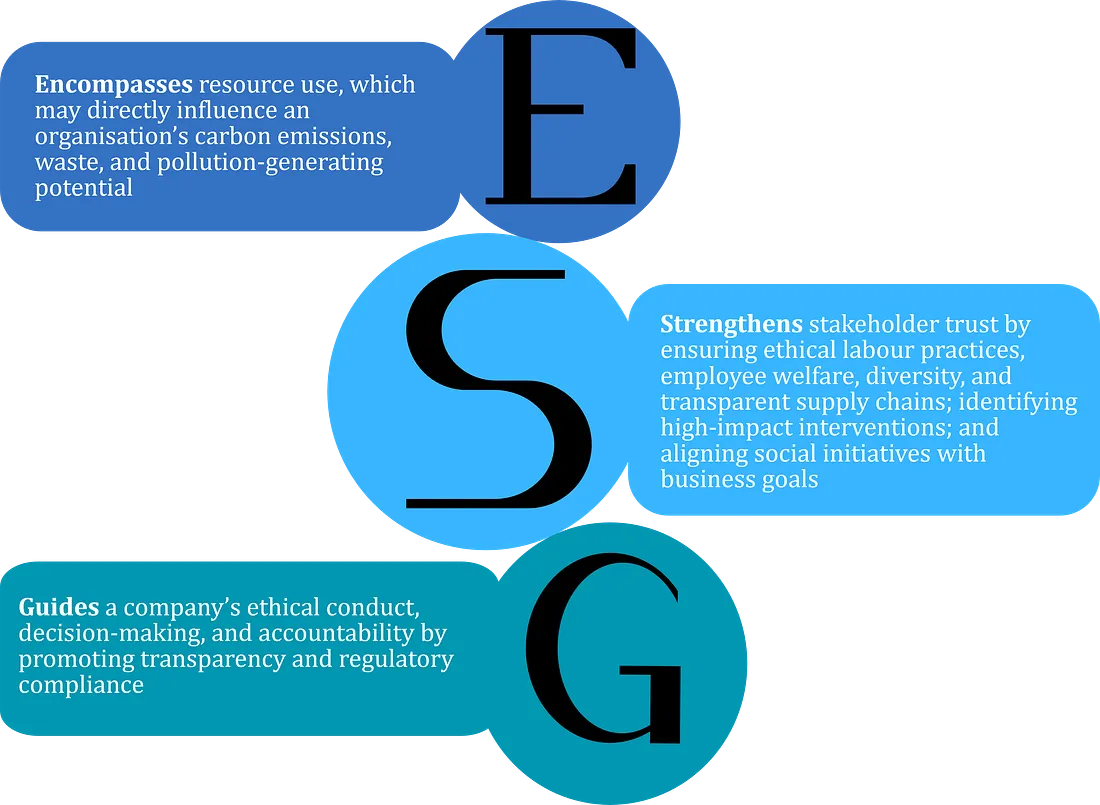

As global scrutiny intensifies and stakeholder expectations rise, Environmental, Social, and Governance (ESG) is evolving from a peripheral concern to a strategic imperative. Expanding on Corporate Social Responsibility (CSR), ESG is a competitive, data-driven strategy that shapes corporate decision-making, prioritising risk management, boosting resilience, enhancing reputation, and driving long-term value creation. For Indian enterprises navigating a dynamic landscape, ESG serves as a blueprint for translating goals into concrete actions for sustainable growth. However, despite this growing significance of ESG, only 27% of Indian organisations are adequately equipped to comply with ESG mandates.

As sustainability gains prominence, Indian enterprises are increasingly prioritising ESG reporting to meet investor expectations, comply with evolving regulations, and align with global standards for transparency and accountability.

One of the most significant regulatory developments in this space is the Business Responsibility and Sustainability Reporting (BRSR), developed by the Securities and Exchange Board of India (SEBI). Now mandatory for the top 1,000 listed companies, it is emerging as the primary ESG disclosure framework in India. Although BRSR covers key ESG parameters, its metrics are specifically tailored to India’s policy and regulatory landscape rather than focussing on sector-specific benchmarks, making it comprehensive in intent but generic in execution. This lack of sectoral granularity can stand in the way of measuring and managing sustainability performance with the precision needed for meaningful impact. Further, BRSR’s strong domestic focus limits its applicability and acceptance at the global level.

Despite growing awareness and regulatory momentum, several systemic gaps continue to undermine the credibility and effectiveness of ESG reporting in India. These challenges not only hamper meaningful sustainability outcomes but also increase the risk of greenwashing. The following are some of the key areas of concern:

To bridge the gaps in BRSR and align with global sustainability standards, many Indian organisations are adopting alternative international frameworks, such as the Global Reporting Initiative (GRI) — widely known for its comprehensive sustainability reporting; the Sustainability Accounting Standards Board (SASB) — preferred for its industry-specific ESG metrics with a major focus on financial performance; and the Task Force on Climate-Related Financial Disclosures (TCFD) — commonly used by manufacturing, finance, and energy companies that face significant climate-related risks.

When implemented with rigour and integrity, ESG can significantly enhance brand reputation, attract investment, unlock new revenue streams, and improve operational resilience. It also enables companies to mitigate long-term risks, particularly those linked to resource scarcity and climate change.

At this juncture, the need for a standardised ESG framework that fosters accountability, transparency, and innovation is undeniable. However, it cannot be considered a silver bullet. To realise the full potential of ESG, the deeper structural issues need to be resolved. We must look beyond checklists and compliance to focus on building institutional capacity and strengthening policy and regulatory ecosystems. Without these measures, ESG risks becoming a superficial label — more about optics than impact. With the right systems in place, ESG can evolve from a box-ticking exercise into a powerful driver of accountability, resilience, and transformative change.

More About Publication |

|

|---|---|

| Date | 16 June 2025 |

| Contributors | |

| Publisher | CSTEP |

| Related Areas | |

Get in touch with us at

cpe@cstep.in